💼 What is PF?

Employee Provident Fund (EPF) is a retirement benefits scheme regulated by the Employees’ Provident Fund Organization (EPFO). It requires both employees and employers to contribute a portion of the employee’s basic salary toward a long-term savings fund, which earns interest and can be withdrawn upon retirement or under specific conditions.

Key Points about PF

- Mandatory for organizations with 10+ employees under the EPF Act.

- Provides financial security post-retirement.

- Every employee is allotted a Universal Account Number (UAN), which remains the same throughout their career.

Bifurcation of Employee and Employer Contribution

| Particulars | Employee | Employer |

|---|---|---|

| EPF | 12% | 3.67% |

| EPS | 0% | 8.33% |

Complete Withdrawal of PF

- PF can be withdrawn upon retirement.

Partial Withdrawal (For Specific Purposes)

- Purchase/Construction/Renovation of house/flat

- Repayment of loan

- Medical treatment of self or family

- Marriage of self/daughter/son/brother/sister

- Post-matric education of children

- Before retirement (after reaching age 54)

- Special cases like closure of company, dismissal or legal challenge

Types of PF and Their Taxability

| Particulars | Recognized PF | Unrecognized PF | Statutory PF | Public PF |

|---|---|---|---|---|

| Employer’s Contribution | Taxable beyond 12% of salary | Not taxable at contribution | Fully exempt | Not Applicable |

| Employee’s Contribution | Deductible u/s 80C (Old Regime) | Not deductible | Deductible u/s 80C (Old Regime) | Deductible u/s 80C (Old Regime) |

| Interest on Employer’s Contribution | Taxable beyond 9.5% p.a. | Not taxable at credit | Fully exempt | N.A. |

| Interest on Employee’s Contribution | Taxable beyond 9.5% p.a. | Not taxable at credit | Exempt up to limit | Fully exempt |

| Withdrawal on Retirement | Exempt u/s 10(12) (See Note 2) | Partially taxable (see explanation) | Exempt u/s 10(11) | Fully exempt u/s 10(11) |

Note 1: Taxability of Interest Amount

- Before April 2021: Entire interest was exempt.

- After April 2021: Exemption only if employee’s annual contribution is ≤ ₹2.5 lakh.

- Where no employer contribution: Exemption limit is ₹5 lakh.

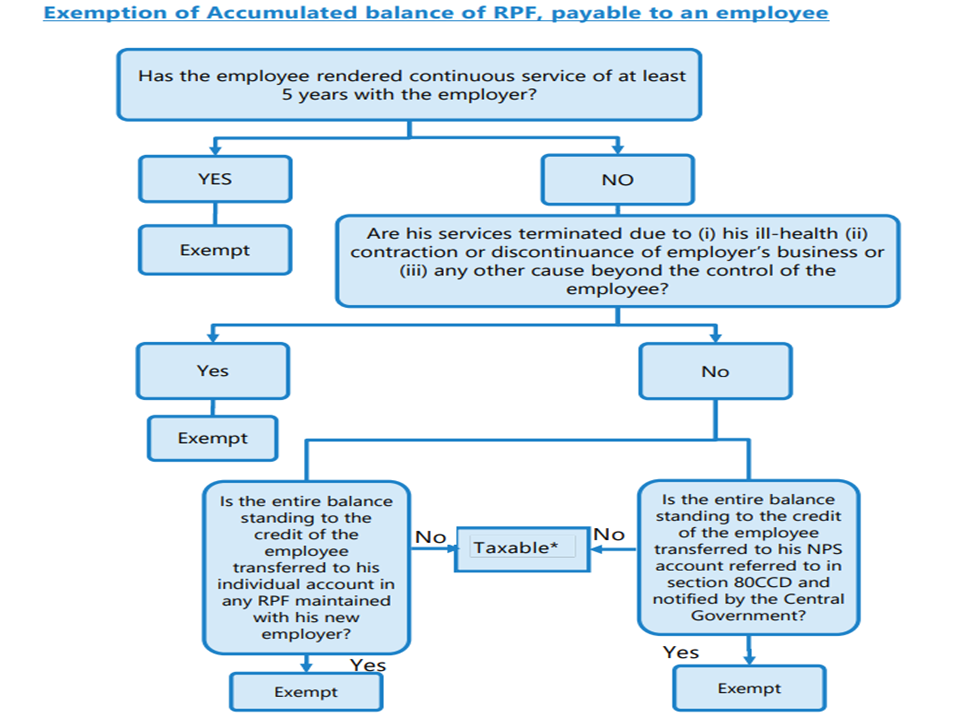

Note 2: Conditions for Exemption of RPF Withdrawal

- Continuous service of 5 years or more

- Termination due to illness, business closure, or unavoidable reasons

- Transfer of PF amount to another Recognized PF

Add comment